Financially Speaking, Would You Opt For a 50 Year Mortgage?

The concept of a 50-year mortgage is gaining interest as banks and policymakers seek solutions to enhance housing affordability.

50 YEARS??? YOU’LL BE GONE BEFORE YOU FULLY OWN YOUR HOME.

Theoretically, a lengthier loan appears to offer advantages: reduced monthly payments, simplified qualifications, and increased “buying power.” However, the numbers and economic principles indicate you’re being duped.

The issue lies in the normalization of 50-year mortgages, which permits housing prices to escalate to increasingly unsustainable levels, leaving homebuyers with no choice but to resort to a 50-year mortgage to afford homes.

If you genuinely wish to assist individuals in purchasing homes, here’s how to do it:

DISCOVER: 20+ Next Crypto to Explode in 2025

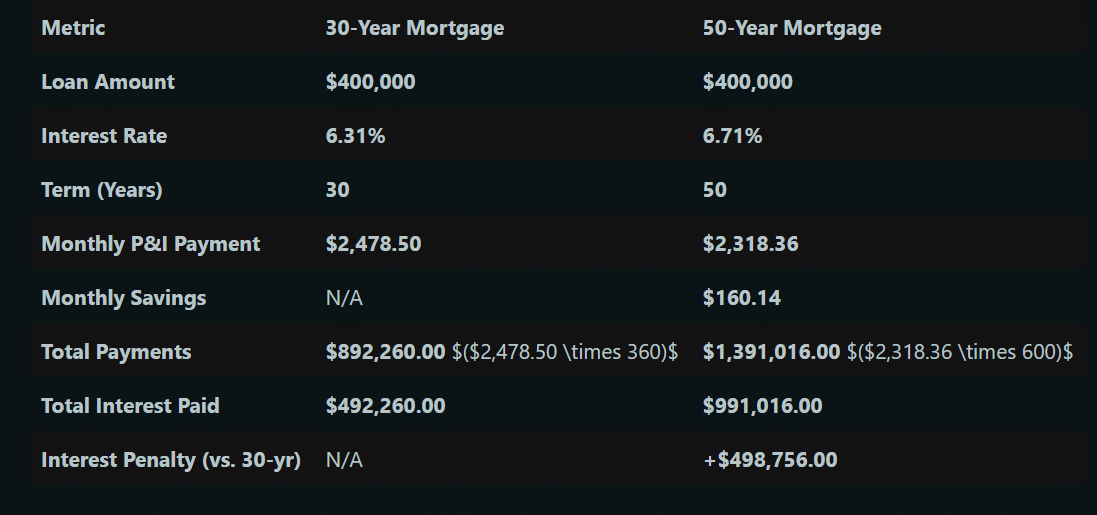

Does The 50-Year Mortgage Math Make Sense?

A loan of $400,000 at 6.31% over 30 years requires $2,478 monthly. Extend that to 50 years at 6.71%, and the payment decreases to $2,318, yielding a mere $160 monthly savings, or roughly 6.5%. SPOILER ALERT: That’s not transformative. However, over the loan’s duration, the borrower ends up paying nearly $500,000 extra in interest.

As per FRED data, the median household income in the US stands at about $79,000 yearly, making a $2,318 mortgage consume over 35% of pre-tax earnings, far exceeding the safe limit for housing expenses.

Boomers with 17 paid-off properties observing you take a 50-year mortgage pic.twitter.com/KkMNAHG4L3

— Not Jerome Powell (@alifarhat79) November 10, 2025

Here’s the catch: Do these vultures in Congress not realize that a 30-year mortgage already encompasses your entire life span?

- Do they not see that mortgages are already spectacularly more beneficial for banks, heavily frontloaded with interest, and equity only begins to build after a minimum of ten years?

- Do they not understand that the average mortgage is paid off only after a few years when individuals sell and relocate?

- Do they not consider the option of refinancing?

You’re better off investing in

BTC

1.95%

BTC

BTC

Price

$104,714.54

1.95% /24h

Volume in 24h

$48.32B

Price 7d

Learn more

or gold and residing in your apartment while those investments appreciate.

DISCOVER: Next 1000X Crypto: 10+ Crypto Tokens That Can Hit 1000x in 2025

Banks Benefit, Buyers Suffer

With a 50-year mortgage, it can take nearly 30 years to amass $100,000 in equity, whereas on a 30-year loan, it’s only about 12 years, per an AP analysis. For the majority of this time, the borrower primarily pays interest, not the principal.

“Prolonging the term doesn’t make homes less expensive,” stated economist Mike Konczal. “It merely establishes debt servitude as the norm for middle-class living.”

Moreover, considering that the typical first-time homebuyer is now approximately 40 years old, according to the National Association of Realtors, a 50-year mortgage would conclude when the borrower reaches 90. Additionally, it doesn’t alleviate the burden of property taxes on that home once you have eventually completed the payment.

“You opted for a 50-year mortgage?”

Indeed, Dave.

“You also chose a 15-year car loan?”

That’s right, Dave. pic.twitter.com/Ndiu3KI0r9

— Not Jerome Powell (@alifarhat79) November 11, 2025

The most effective solution to the housing crisis is to limit lending to around triple the annual salary, causing home values to plummet overnight. Builders would have to shift to constructing affordable homes to remain viable instead of high-priced McMansions.

This will most likely never occur, as banks would face a substantial profit drop, and boomers would be enraged that the home they purchased for $50k in 1988 is now valued at only $200k instead of $600k.

DISCOVER: Top 20 Crypto to Buy in 2025

Is Trump The Biggest Scam President?

According to FRED and Zillow Research, home prices in the US have surged by 44% since 2020, while real wages have barely changed.

This 50-year mortgage proposal from Trump, paired with his 15-year car loan, appears to be rooted in desperation rather than sound policy.

The utmost, and we stress utmost best-case scenario is that the value of the home you’re mortgaged on increases over time and turns into pure profit when sold.

If a house’s value doubles in 15 years, when you sell, the increased amount becomes your cash. But this scenario means you’re speculating on a housing trading market that is already excessively high, unstable, and potentially in a bubble.

EXPLORE: Singapore Denies Do Kwon’s $14M Refund Market demand For ‘Stolen’ Penthouse

Join The 99Bitcoins Announcement Discord Here For The Latest Trading market Updates

Key Takeaways

- The concept of a 50-year mortgage is gaining interest as banks and policymakers seek solutions to enhance housing affordability.

- Best case scenario is that whatever amount the house you’re paying a mortgage on appreciates over time

The post Financially Speaking, Would You Sign Up For a 50 Year Mortgage? appeared first on 99Bitcoins.

moment to excel?")